HitPay’s pitch is “no monthly fee, everything included”: FPX, cards, seven-plus wallets, DuitNow QR, BNPL and built-in recurring billing behind one dashboard. The pricing is genuinely published, but it has more moving parts than a flat-fee gateway, and one add-on is easy to miss.

The base rates

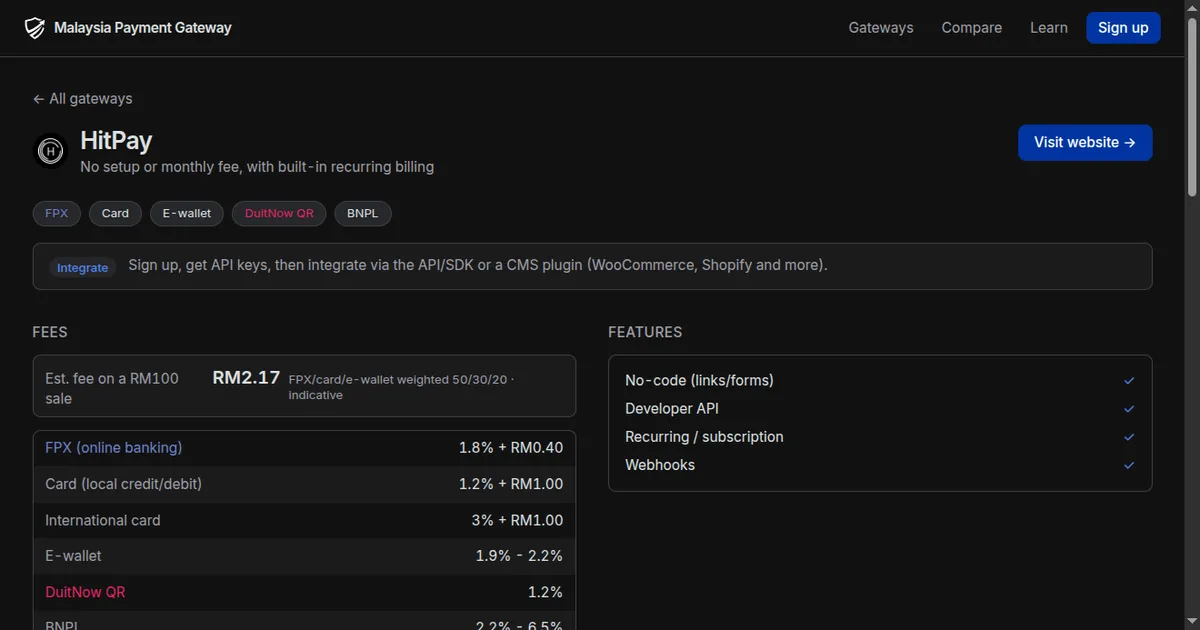

From the official Malaysian pricing page:

- Local cards: 1.2% + RM1.00, one of the lowest published card rates in the directory.

- FPX: 1.8% + RM0.40.

- DuitNow QR: 1.2%.

- International cards: 3% + RM1.00, plus 2% on foreign-currency transactions.

- E-wallets, per wallet: Touch ’n Go 1.9%, GrabPay 2%, Boost 2.1%, Maybank QRPay 2.1%, ShopeePay 2.2%.

- BNPL: SPayLater 2.2%, Atome 5.5% + RM1, PayLater by Grab 6.5%.

The add-on people miss

Some HitPay products carry a platform fee on top of the channel rate: 0.2% on payment links, invoicing and the online store, and 0.5% on the Shopify app. It is small, but on thin margins it matters, and it is the difference between the headline rate and what lands in your reconciliation.

Settlement runs T+2 for most channels; cards start from T+3 because HitPay’s card processing runs on Stripe rails.

Where HitPay actually wins

Two things stand out against the cheap-FPX crowd. First, that 1.2% + RM1 card rate: on a RM300 ticket it is RM4.60, where 3% gateways charge RM9 or more. If cards dominate your mix, HitPay’s blend gets competitive fast; check your split in the fee calculator.

Second, recurring billing is included. Most low-cost Malaysian gateways skip card-on-file charging entirely, so subscription businesses usually face a jump to enterprise pricing. HitPay sits in that gap, alongside the other recurring-capable gateways.

The trade-off is FPX: 1.8% + RM0.40 loses to flat-fee providers on bigger tickets. RM1.00 flat beats it from about RM34 upward, which is exactly the comparison in HitPay vs toyyibPay. Full profile: HitPay.